As a result of the SECURE 2.0 Act, the age to start taking RMDs increased from 72 to 73 beginning in 2023 and will increase to 75 in 2033. If you turn 73 between now and 2033, you must begin taking RMDs by April 1st of the year following the year in which you reach age 73 or separate from service (whichever is later).

You will receive communication from the ABA Retirement Funds Program (“Program”) before the year in which you must begin taking RMDs. Once RMDs are required to be paid from your account, the Program will calculate the amount you are required to take and pay out to you each year thereafter by December 31.

Here are some frequently asked questions about RMDs to help you know what to expect:

Here are some frequently asked questions about RMDs to help you know what to expect:

Q. Who is required to take an RMD?

A. A participant who has attained age 73 and who (a) is no longer working* for the firm that sponsors their retirement plan or (b) continues working for the employer that sponsors his/her retirement plan and owns 5% or more of the employer entity at any time during the calendar year in which he/she turned 73.

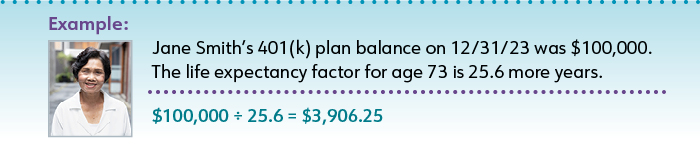

Q. How is my RMD calculated?

A. Your RMD is based on your prior year-end account balance (excluding the balance from a designated Roth account*)** divided by the applicable life expectancy factor according to the IRS’s Uniform Lifetime Table.

Q: Do I owe taxes on my RMD? Will any taxes be applied?

A. Yes. Generally, RMDs are treated as ordinary income for income tax purposes. You have the ability to provide withholding instructions to the Program. If you do not provide withholding instructions, the Program will automatically withhold 10% in federal income tax, as well as any applicable state tax.

Q: Can RMDs come directly out of my Schwab Personal Choice Retirement Account® (“PCRA”)?

A. RMD payments cannot be made directly from the PCRA. Instead, you must make sure that you have enough assets in the Program’s core investment options to cover the total withdrawal, which may mean liquidating securities. The Program’s Customer Service Associates at 800.348.2272 can help you determine if this liquidation will be necessary. If PCRA funds are not moved prior to the RMD sweep, you will need to transfer the necessary funds to the core investment options and then request an RMD by submitting the Required Minimum Distribution Form.

Q: Can I choose not to take my RMD?

A. If you don’t take any distributions, or if the distributions are not large enough, you may have to pay a 25% excise tax on the amount not distributed as required; however, the excise tax is reduced to 10% if the proper amounts are withdrawn within 2 years. The Program will issue your first RMD in mid-March following the later of the year during which you (a) turned 73 or (b) terminated employment with the employer entity which sponsors the retirement plan in which you participate and will issue each RMD thereafter in early December through an automatic sweep from your core fund balance.

Q: Can I aggregate the RMD amounts for all of my retirement plan accounts and Individual Retirement Accounts (“IRAs”) and withdraw the total RMD amounts from one account?

A. No. The RMD from your retirement accounts must be calculated and satisfied separately for each plan. Although you can aggregate the RMD amounts to be paid from your IRAs (if you have an IRA), this aggregation rule does not apply to your retirement plan account in the Program.

Please note: It is important to complete the initial RMD questionnaire sent out to you before the year in which you must begin taking RMDs and to review the periodical RMD confirms you receive thereafter for accuracy. If you have any questions about RMDs, please reach out to the Program at 800.348.2272 or contactus@abaretirement.com.

* With Roth 401(k) contributions, you pay your taxes upfront – at your current tax rate – but do not pay taxes on qualified distributions of contributions and any investment earnings. A qualified distribution requires you to be age 59 1/2 or older. A qualified distribution may be taken if you become disabled or can be made to your beneficiary(ies) after your death. In addition, a qualified Roth distribution requires you meet one of the criteria above, and the funds must be held for a 5-year holding period dating from the earlier of: a) the first year of your Roth contribution, or b) if you make a direct rollover from another plan with a designated Roth account, the first year you made a Roth contribution to that plan which the direct rollover originated. To learn more about the differences between traditional pre-tax contributions and Roth contributions, review the Program’s Contribution Options Guide.

** While the original owner does not need to take RMDs from a Roth account, beneficiaries inheriting a Roth account may have to take required minimum distributions based on their own life expectancy.

RELATED POSTS: