How can you plan to help pay for eligible health care costs today and well into your future?

How can you plan to help pay for eligible health care costs today and well into your future?

A Health Savings Account (“HSA”) may help you save. Individuals who are covered under a high deductible health plan (“HDHP”) have the option to have an HSA. An HSA balance can be used to pay qualified medical expenses today, tomorrow and throughout your retirement years. Your balance carries over from one year to the next – it does not expire. Once you have reached a minimum balance in your account (your plan’s investment threshold), you have the option of investing a portion of your balance in your HSA’s investment lineup. As with any investment, there are risks; make sure to fully explore those risks before choosing to invest.

How much can you save?

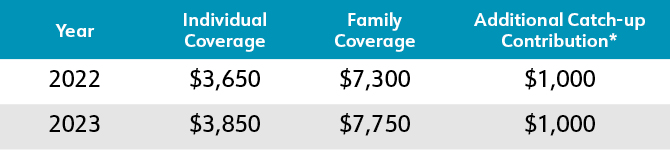

If you have an HSA, the Internal Revenue Service recently increased the HSA contribution limits for 2023.

HSA Contribution limits

Whether you enrolled as an individual within your HDHP or maintain family coverage will determine how much you can contribute to your HSA:

* The catch-up contribution is for HSA owners who are turning age 55 or older on or before Dec. 31 of the calendar year during which contributions are made.

Remember, you can make your 2023 HSA contributions between Jan. 1, 2023, and the date your federal income tax is due, which will be Monday, April 15, 2024.

Don’t have an HSA?

If you have an HDHP but don’t yet have an HSA, here are some factors that you may want to consider:

- Once you reach your plan’s investment threshold, money in an HSA can be invested, with a potential for investment returns that will compound tax-free and increase the value of the account. As with any investment, there are risks; make sure to fully explore those risks before choosing to invest

- Earnings within the HSA account are not subject to taxes on a year-to-year basis

- An HSA doesn’t have required minimum distributions. You can choose to save money in an HSA during your working years, then take tax-free distributions from your balance to pay for qualified medical expenses in retirement, at a time when those expenses may be higher

- Distributions for qualified medical expenses including expenses not covered by Medicare are tax-free (other distributions are subject to ordinary income tax and, before age 65, an additional 20% IRS penalty tax)

Click here to access the IRS Revenue Procedure announcing the 2023 HSA contribution limits: RP-2022-24 (irs.gov)